Ana Santos Rutschman at Saint Louis University Law School has authored an interesting short article titled, "Why Moderna Won't Share Rights to the COVID-19 Vaccine with the Government that Paid for Its Development" in The Conversation. The article basically outlines the U.S. government's technical and monetary contributions to the development of the mRNA technology and a dispute between Moderna and the U.S. government. The article is available, here. Moderna's stock has been falling overall, and I imagine this will not help as this is resolved. I've been worried about vaccine availability for some time, but I didn't realize so many would choose not to be vaccinated. It appears COVID-19 mutation will continue relatively unabated.

Saturday, 20 November 2021

Friday, 12 November 2021

The TRIPS Trap Revisited

By Roya Ghafele, OxFirst

The World Trade Organization’s Trade-Related Aspects of Intellectual

Property Rights (TRIPS) Agreement forced much of the

developing world to adopt minimal standards for intellectual property (IP) protection.

The imposition of such standards has been subject to much criticism. NGOs and

advocates of international development have raised serious concerns about TRIPS,

TRIPS Plus (which expands existing obligations under TRIPS), and the increasing

use of bilateral trade agreements to expand IP protection.

Critics of such agreements cite the costs associated with

enacting IP legislation and that, due to global IP protection, imitation as a

development strategy has been ruled out. These concerns can neither be denied,

nor is it the aim of this article to dismantle them. They are certainly important problems that

deserve to be further studied.

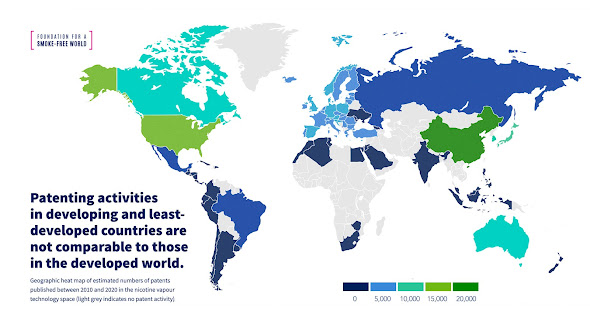

However, preliminary insights in the patent positions in

technologies relating to tobacco harm reduction suggests that out of 74 000

patents published on technologies aiming to reduce the harm of smoking, hardly

any cover the developing world.

With the exception of South Africa, the typical African

country has not seen any significant patent filings in this technology.

Figure 1: Indications of patents relating to vaping over

the last decade

There may certainly be conditions lying outside of the patent system that have discouraged tobacco companies from creating IP in these countries. However, the significant difficulties developing countries may have faced with implementing the patent system, may also have discouraged patenting activities in the developing countries.

Many developing countries have struggled setting up

functioning patent offices, finding qualified staff, training judges in IP and

developing local IP professionals. in some countries patent offices may have

been established without the necessary infrastructure or human capacity to

successfully examine patent applications. IP legislation has been enacted

without investing in the necessary infrastructure to turn legal theory into

legal practice. None of this may have been undertaken in bad faith or to

wilfully breach a commitment to international trade.

Rather, the sad reality is that in many developing

countries there is very little understanding about IP and its economic impact. Even

at the European level, the qualifying exam for European patent attorneys is

more successfully passed by Brits or Germans, rather than their colleagues from

less-privileged countries. Greece, for example, has up until now not succeeded

in developing patent attorneys and the job is undertaken by lawyers.

Lack of know-how and know-why, are probably the primary

reasons many developing countries are still grappling with the IP system. Leading

IP economies have often been less than understanding about the constraints

facing developing nations. The Office of the US Trade Representative for

example releases annually a special report on IP and review of notorious

markets for counterfeiting and piracy.

International development aid for IP has been rather scattered.

The World Intellectual Property Organization (WIPO) followed the United States

Agency for International Development (USAID) offer the most important support

for IP-related development assistance. However, at the international level technical

assistance can often be neither coordinated nor continuous. With the exception

of WIPO, such assistance may also have a tendency to reflect the specific

requirements of the bilateral donor country, rather than focus on the larger

needs of a developing country or an entire region.

All of this has led to the current sorry state of global IP

law. While some nations are at the forefront of defining the technology law of

the future, others are still confronted with a situation where ordinary people

have probably not even heard of intellectual property.

The initial analysis in the tobacco space was a harsh

awakening as to how at least one sector of the economy assesses the value

proposition of developing countries’ IP systems. Tobacco companies are waging

trans-jurisdictional patent battles over next-generation tobacco products, but

at the same time their focus on developing country IP is minimal.

This is at odds with the market reality. Over 85% of

smokers live in developing countries, yet the patent focus remains on developed

nations. The market potential for tobacco harm-reducing products in developing

nations is substantial, if these products were to be made available globally,

rather than to consumers in developed countries only. This would not only

expand business opportunities for the tobacco industry, but would also offer people

around the globe less harmful ways to consume tobacco. A potential “win-win”

situation is being hampered by a deplorable implementation of the patent system

in many countries.

I do not want to be misunderstood as a hard-core advocate

of the patent system. However, the initial patent landscape analysis made me

wonder if in the 21st century any nation can truly afford to stay outside of

that system. The reality is that, doing so, translates into marginalization. This

segregation may be so pronounced that companies may not be motivated to invest

in patents in these countries. Usually, this also means that they have no

intention of selling patented products in these countries, leading to restricted

consumer choice and limited take-off of technology. Whether this is indeed a

better development choice should be a subject of further discussion.

Key words: smoking, tobacco hard reduction, patent protection, low- and middle-income countries

Disclosure of Conflict of Interest: OxFirst has been compensated by the Foundation for a Smoke-Free World, the views are

the author’s own. The preliminary patent landscape report is available here and here.

Saturday, 6 November 2021

U.S. DOJ Settles Generic Drug Price Fixing Cases -- Over $400 million

The U.S. Department of Justice has settled several lawsuits concerning essentially of illegal price fixing between companies offering generic drugs. This is a continuation of the problems facing drug pricing and the generic market. Government production of generics may be the future. The U.S. Department of Justice press release states, in part:

Three generic pharmaceutical manufacturers, Taro

Pharmaceuticals USA, Inc., Sandoz Inc. and Apotex Corporation, have agreed to

pay a total of $447.2 million to resolve alleged violations of the False Claims

Act arising from conspiracies to fix the price of various generic drugs. These

conspiracies allegedly resulted in higher drug prices for federal health care

programs and beneficiaries according to the Justice Department.

The government alleges that between 2013 and 2015, all three

companies paid and received compensation prohibited by the Anti-Kickback

Statute through arrangements on price, supply and allocation of customers with

other pharmaceutical manufacturers for certain generic drugs manufactured by

the companies.

Taro Pharmaceuticals USA, Inc., headquartered in New York,

has agreed to pay $213.2 million. The Taro drugs allegedly implicated in this

scheme address a wide variety of health conditions, and include etodolac, a

nonsteroidal anti-inflammatory drug used to treat pain and arthritis, and

nystatin-triamcinolone cream and ointment, a combination of an antifungal

medicine and steroid used to treat certain kinds of skin infections.

Sandoz Inc., headquartered in New Jersey, has agreed to pay

$185 million. The Sandoz drugs at issue include benazepril HCTZ, used to treat

hypertension, and clobetasol, a corticosteroid used to treat skin conditions.

Apotex Corporation, headquartered in Florida, has agreed to

pay $49 million in connection with its sale of pravastatin, a drug used to

treat high cholesterol and triglyceride levels.

“Illegal collaboration on the price or supply of drugs

increases costs both to federal health care programs and beneficiaries,” said

Acting Assistant Attorney General Brian M. Boynton of the Justice Department’s

Civil Division. “The department will use every tool at its disposal to prevent

such conduct and to protect these taxpayer-funded programs.”

“These civil settlements are another achievement in my

office’s efforts to hold generic drug companies accountable for the consequences

arising from price-fixing schemes, including the harm to federal health care

programs,” said Acting U.S. Attorney Jennifer Arbittier Williams for the

Eastern District of Pennsylvania. “We will continue to aggressively pursue

these violations of the Anti-Kickback Statute and the False Claims Act and

obtain significant recoveries.”

“Conspiring to raise prices on generic medications is illegal

and could prevent patients from being able to afford their needed prescription

drugs. Americans have the right to purchase generic drugs set by fair and open

competition, not collusion,” said Special Agent in Charge Maureen R. Dixon of

the Philadelphia Regional Office of the Inspector General, Department of Health

and Human Services (HHS-OIG). “HHS-OIG along with our law enforcement partners

will continue to investigate allegations of companies engaging in actions that

put the public and the Medicare program at risk.”

In connection with its settlement agreement, each company

also entered a five-year corporate integrity agreement (CIA) with OIG. The CIAs

include unique internal monitoring and price transparency provisions. They also

require the companies to implement compliance measures including risk

assessment programs, executive recoupment provisions and compliance-related

certifications from company executives and board members. . . .

The Anti-Kickback Statute prohibits companies from receiving

or making payments in return for arranging the sale or purchase of items such

as drugs for which payment may be made by a federal health care program. These

provisions are designed to ensure that the supply and price of health care

items are not compromised by improper financial incentives. These settlements

reflect the important role of the False Claims Act to ensure that the United

States is fully compensated when it is the victim of kickbacks paid to further

anticompetitive conduct.

All three companies previously entered into deferred

prosecution agreements with the Antitrust Division to resolve related criminal

charges. Taro paid a criminal penalty of $205.6 million and admitted to

conspiring with two other generic drug companies to fix prices on certain

generic drugs. Sandoz paid a criminal penalty of $195 million and admitted to

conspiring with four other generic drug companies to fix prices on certain

generic drugs. Apotex paid a criminal penalty of $24.1 million and admitted to

conspiring to increase and maintain the price on pravastatin. The civil

settlement payments announced today are in addition to the criminal penalties

paid by the companies.

The press release is available,

here.

Thursday, 4 November 2021

Morrison and Foerster Sponsors Webinar titled, "In a Founders Market, Strategic Capital Thrives."

The law firm Morrison & Foerster (a very famous law firm based in California known as MoFo) is sponsoring a free webinar on the “buyer’s market” for capital titled, “In a Founders Market, Strategic Capital Thrives.” The webinar is scheduled for “Tuesday, November 16, 2021[,] 9:00 a.m. – 10.00 a.m. PT[,] . . . 5:00 p.m. – 6:00 p.m. GMT.”

Additional details are below:

|

2021

is turning out to be a record-setting year for investment in VC-funded

startups and private companies. This vast global liquidity has caught the

eyes of non-traditional investors including sovereign wealth funds and

limited partners, both of whom are looking to boost returns with direct investments. This makes it a

buyer’s market for startups, and the best entrepreneurs have access to what

seems like unlimited capital.

Panelists Include:

|

RSVP is available, here.

Wednesday, 3 November 2021

U.S. FDA Sends Letter to Push USPTO Concerning Drug Patents and Access

The U.S. Federal Food and Drug Administration (FDA) recently sent a letter to the U.S. Patent and Trademark Office concerning the FDA’s concerns regarding pharmaceutical patents and their impact on innovation and access. Some of the concerns include the use of continuations to build patent thickets to raise litigation costs as well as resulting in possible delays of generic entry; evergreening practices; and product-hopping. Notably, the FDA is generally interested in increasing communication and collaboration to address those issues, including offering expertise, collecting additional information regarding IPRs and other post-grant procedures as well as inquiring whether examiners need more time to review patent applications. While the Trump Administration also had concerns regarding drug pricing, President Biden’s recent Executive Order concerning competition is the impetus for this letter’s push for increased collaboration.

U.S. Federal Trade Commission Releases New Safeguards Rule for Non-Banking Financial Institutions

The Federal Trade Commission (FTC) in the United States has changed the regulations concerning the Safeguards Rule relating to cybersecurity standards for non-banking financial institutions. Essentially, the new Safeguards Rule contains additional specificity regarding what is required to comply with the contextual administrative, physical and technical standards for a compliant information security program. The new Safeguards Rule will be effective a year from publication in the Federal Register. Notably, the new Safeguards Rule contains significant new definitions. The FTC press release states, in relevant part:

The FTC’s updated Safeguards Rule requires non-banking

financial institutions, such as mortgage brokers, motor vehicle dealers, and

payday lenders, to develop, implement, and maintain a comprehensive security

system to keep their customers’ information safe.

“Financial institutions and other entities that collect

sensitive consumer data have a responsibility to protect it,” said Samuel

Levine, Director of the FTC’s Bureau of Consumer Protection. “The updates

adopted by the Commission to the Safeguards Rule detail common-sense steps that

these institutions must implement to protect consumer data from cyberattacks

and other threats.”

The changes adopted by the Commission to the Safeguards

Rule include more specific criteria for what safeguards financial

institutions must implement as part of their information security program such

as limiting who can access consumer data and using encryption to secure the

data. Under the updated Safeguards Rule, institutions must also explain their

information sharing practices, specifically the administrative, technical, and

physical safeguards the financial institutions use to access, collect,

distribute, process, protect, store, use, transmit, dispose of, or otherwise

handle customers’ secure information. In addition, financial institutions

will be required to designate a single qualified individual to oversee their

information security program and report periodically to an organization’s board

of directors, or a senior officer in charge of information security.

The Safeguards Rule was mandated by Congress under the 1999

Gramm-Leach-Bliley Act. Today’s updates are the result of years of public

input. In 2019, the FTC sought

comment on proposed changes to the Safeguards Rule and, in 2020

held a

public workshop on the Safeguards Rule.

In addition to the updates, the FTC is seeking comment on

whether to make an additional change to the Safeguards Rule to require

financial institutions to report certain data breaches and other security

events to the Commission. The FTC is issuing a supplemental notice of proposed rulemaking,

which will be published in the Federal Register shortly. The public will have

60 days after the notice is published in the Federal Register to submit a

comment.

The new Safeguards Rule is available, here. Notably, there is legislation before the U.S. Congress to massively increase the budget of the FTC to deal, in part, with privacy and cybersecurity issues.

Thursday, 30 September 2021

Essentiality Rate Inflation and Random Variability in SEP Counts with Sampling and Essentiality Checking for Top-Down FRAND Royalty Rate Setting

Fair, reasonable and non-discriminatory (FRAND) royalty rates for licensing standard-essential patents (SEPs) are increasingly derived “top-down” by dividing a notional aggregate royalty percentage (e.g., 10% of a smartphone’s selling price for 4G LTE) among patent owners based on the proportions of patents they own that are deemed to be standard essential.[1] Other rate-setting methods include use of comparable licenses and measuring value derived from SEPs. However, as stated by Justice Birss in Unwired Planet: “In assessing a FRAND rate counting patents is inevitable.”[2] He used top-down methodology as a cross check. The FRAND rate Decision in TCL v. Ericsson, that was unanimously and entirely vacated on appeal, also relied on a top-down valuation.[3]

|

| Ball colour, not patent essentiality, can be identified with 100% accuracy when sampling |

Essentiality checking is also proposed by the European Commission

and others to improve transparency for prospective licensees.[4] But transparency is only legitimate if what

is being revealed and counted is reasonably accurate and does not mislead.

Otherwise, it will likely do more harm than good.

If patent counting with essentiality checking is going to be used

in FRAND-rate determinations, then it is vital we understand its dynamics,

failings, how to properly interpret its results, and how to design and size

essentiality determination studies that are fit for purpose. This research

article contributes to that quest.

Figuring out which patents are true SEPs and then counting

them is fundamental to top-down analysis. With hundreds of thousands of patents

declared possibly standard essential,[5]

and the insuperably huge task in checking them all for essentiality, the

European Commission and others propose that assessing only samples of patents declared essential

to a standard would suffice.

Institutionalising use of patent counting—with or without sampling—is an under-researched and impetuous leap of faith. Different assessors come up with wildly different patent counts. Comparison of two separate assessors determining essentiality on the same sample of patents indicates that assessors tend to inflate true essentiality rates. These over-estimates result from statistical bias with numbers of false positives (i.e., truly not essential patents being found to be essential) exceeding false negatives when true essentiality rates are rather less than 50%.

I also conclude from my simulation modelling and analysis that:

1. The lower the true essentiality rate and the lower the rate of agreement among different assessors, the larger the differences will be between the essentiality rates determined by assessors and the true essentiality rate. For example:

a. If true essentiality rates are 30% and two different assessors agree with each other on 75% of their determinations, they will tend to estimate 36% essentiality rates and be accurate in 85% their determinations.

b. If true essentiality rates are only around 10% (e.g., for 4G LTE or 5G), as some experts plausibly argue, and if two assessors agree with each other on 84% of their determinations, they will tend to estimate 17% essentiality rates and be accurate in 91% of their determinations. That means there will be nearly as many false positives as correct determinations of essentiality.

2. Therefore, if true essentiality rates are at the lower end of expectations, for example, at around 10% or less, it is imperative assessors are highly accurate in their determinations, otherwise false positives will swamp their correct determinations and make their overall results meaningless.

Sampling reduces the precision of SEP counts with increased variability, which is exacerbated by erroneous essentiality determinations. Sampling theory and simple simulations using results of patent-counting studies already undertaken—including several with sample sizes below a few hundred—reveal unacceptably large ranges in expected essentiality rate determinations (i.e. the percentage of declared-essential patents that are deemed to be essential)[6] at what various study authors regard as the “well accepted bound” of the 95% confidence level.[7] This variability is particularly large where patent essentiality rates are at low levels, such as at around 10%. For example, 10% ± 1.5% is actually ± 15% variability as a proportion of that 10% figure. The quantitative analysis I undertook for this article measures the extent of diminutions, which should be properly and fully considered before sample sizes are set, and before the short cut of sampling is blindly adopted at all.

Top-down methodology seemingly enables precise assessments of

FRAND royalties, but this is an illusion due to various inconsistencies and

inaccuracies in patent selection, sampling and essentiality assessment. Key

questions are how much precision is adequate and how can that be obtained? The

optimal balance between extensive and costly patent-essentiality assessments, that

can take days of work per patent, versus reducing the number of assessments by

sampling should be decided with due regard to accuracy and confidence levels required,

and based on empirical assessments.

While there are no set bounds for the acceptably accurate

range in determinations, I have considered a reasonable proportionate accuracy requirement

for essentiality rate determination to be <± 15% (i.e., a 30% range for the determined

essentiality rate as a proportion of the true essentiality rate) at the 95%

confidence interval level. With my opinion that true essentiality rates are

more like 10% than 30% or 40%, I conclude from my analysis that samples including thousands of patents are

required in top-down FRAND-royalty rate setting. For example, if the

essentiality rate is only 10%, a sample size approaching 3,000 declared-essential

patents per standard, at the very least, would be required.

My full article, including detailed statistical analysis, can be downloaded here.

[1]

These percentages in mobile phone licensing are typically applied to the

wholesale selling prices of finished goods products.

[2] Approved Judgment in Unwired Planet versus

Huawei, 5th April 2017 at 806 (11). https://www.judiciary.uk/wp-content/uploads/2017/04/unwired-planet-v-huawei-20170405.pdf

[3] http://www.ip.finance/2018/04/unreasonably-low-royalties-in-top-down.html

and https://www.reuters.com/legal/transactional/ericsson-tcl-settle-long-running-smartphone-patent-disputes-2021-07-19/

[4] https://ec.europa.eu/growth/content/transparency-sep-licensing-how-clarify-possible-exposure-upfront_en

[5] Declaring

one’s patents that are possibly standard essential is a requirement for

participation in organisations such as 3GPP in the setting of standards such as

4G LTE and 5G.

[6] This is

also called the essentiality ratio.

Tuesday, 7 September 2021

Modest SEP royalties on smartphones have declined and licensing is stabilizing

Aggregate royalty payments for licensing cellular technology standard-essential patents (SEPs) in smartphones have remained in modest single-digit percentages and have declined since 2013.

This defies

purported concerns that the stacking of patent royalties paid to multiple

licensors has led to or would lead to unreasonably high aggregate rates on

mobile devices. It also counters the claims of some original equipment manufacturers (OEMs) and others that

various SEP owners demand licensing fees in excess of what is fair, reasonable

and non-discriminatory (FRAND).

The true aggregate price is fair and reasonable

Amid wild

speculation about SEP licensing charges up until 2015, one article drawing a

lot of attention around then outrageously asserted the cost could be 30 percent

of a $400 smartphone price. In response, I set about measuring how much in

patent royalties was actually being paid in comparison to total revenues generated

on mobile handset sales (e.g. $410 billion in 2014, according to IDC). I termed

the ratio of the two figures, expressed as a percentage, the “royalty yield.”

This is an average reflecting all royalties paid divided by the total of licensed

and unlicensed handset sales revenues. I found the royalty yield to be no

more than around 5 percent in aggregate including all licensors. That percentage is

the sum of the royalty yields for individual licensors.

My

assessments were conservatively high because some of the royalties paid are for

licensing intellectual property other than cellular SEPs, or are for network

equipment, devices such as PC data sticks or IoT appliances.

I found

that major licensors Alcatel-Lucent, Ericsson, InterDigital, Nokia and Qualcomm

accounted for most royalties paid, even with conservatively high estimates for

other licensors. For example, I included 3G and 4G LTE patent pool licensing at

rate card prices, even though it was evident hardly any implementers were

signing up for those.

My

methodology and results were replicated and validated in a couple of academic research papers, including

one enduring peer review before publication, which with more detailed analysis showed aggregate

yields to be even lower than my estimates.

Aggregate royalties declined despite global boom in 4G LTE smartphones and introduction of 5G

Total royalties and royalty yields have fallen substantially since 2015 for those major cellular SEP licensors. While 4G LTE smartphone sales surged, OEMs have managed to reduce royalty rates paid for licensing. For example, even though royalties are generally charged as a percentage of a phone’s selling price, royalty caps limiting the royalty charge—as if the phone price was, for example, $200 or $400—ensure that royalty yields reduce as smartphone prices are raised, for example, with introduction of new models priced at $1,000 or more in recent years.

Licensing

revenues and aggregate royal yield for major mobile SEP licensors

2013-2020

Source: Company financial disclosures and

WiseHarbor analysis.

Nokia completed its acquisition of Alcatel-Lucent in 2014.

Qualcomm figures include retroactive allocations of licensing dispute settlement

payments of $4.7 billion by Apple in 2019 and $1.8 billion by Huawei in 2020

that were not included in Qualcomm Technology Licensing segment figures.

With the

introduction of each new generation of mobile technology since 3G, it was also

alleged that charges for the new standards would stack further to an

unreasonable aggregate burden on OEMs and consumers. However, despite 5G’s

commercial introduction in 2019, aggregate royalties have not risen for these

companies that also first announced programs and charges for 5G licensing.

Up and downs

There is

was substantial increase in royalty income for Nokia from 2014. But this is

unsurprising due to a dramatic change in the company’s industry profile and

business model following the divestiture of its smartphone business to

Microsoft that year. For Nokia prior to 2014, as for Samsung and Apple since

then, SEP licensing was more oriented to minimizing—through cross-licensing—the

licensing fees charged by other patent owners on market-leading handset sales,

than to generating cash royalties. A question posed to me by a hedge fund

client back then was: ‘to what extent and how quickly could Nokia “unroll” its

cross-licenses to increase the cash royalties it receives?’ Nokia’s licensing

revenues more than doubled between 2014 and 2017 before declining around 15 percent

in the following years to 2020. The company’s royalty yield also doubled to 0.4

percent before falling back somewhat over the same time periods.

Though

royalty fees for Ericsson, Nokia and Qualcomm are modest in comparison to

revenues from all their other sales, royalties are very important because profit

margins on licensing are relatively high. SEP licensing fee income is crucial

to fund the substantial ongoing R&D investments by all these licensor

companies, also including InterDigital. With development of further

standard-essential technologies, the benefits of those investments also become openly

available to the entire mobile ecosystem.

The major

licensors detailed in my 2015 analysis received more than half of all royalties

paid and still do despite the overall decline in licensing revenues for these

companies. The aggregate royalty yield including the above-named companies and

all other licensors has also declined. As other players have become more

significant in licensing, these have had only minor effects on aggregate royalties

paid by OEMs to all licensors. For example, while Huawei now boasts large

shares of patents declared essential to LTE and 5G standards, with its

smartphone market share second only to Samsung in 2019, like old Nokia, Samsung

and Apple, Huawei has also been more focused on minimizing the royalties it has

had to pay out than on increasing the cash royalties it generates. With

cross-licensing, OEMs with SEP portfolios share their intellectual property

while minimizing licensing costs on their product manufactures and sales.

With the US chip supply bans on Huawei and with it

spinning off its Honor sub-brand, Huawei’s smartphone market share has plummeted and it is also now seeking

to increase its patent monetization. While Huawei has reportedly paid out

more than $6 billlion in patent fees over decades, it is expecting to generate

between $1.2 billion and $1.3 billion in patent licensing revenues between 2019

and 2021. I presume

that means revenues averaging around $420 million per year over three years.

Similarly, with LG exiting the smartphone market due to its poor profitability there,

despite its large mobile SEP portfolio, it could also seek to increasingly

monetize its SEPs through licensing, or through patent sales.

There are

other cellular SEP licensors, including some so-called patent assertion

entities that have obtained headline-grabbing licensing awards. But the

significance of these on aggregate royalty yields is also relatively small. Large

award figures tend to cover numerous years of infringement and it can take many

years of litigation with awards being amended or revoked before appeals

processes are exhausted or settlement with lower amounts paid. Following the annulment

of a $506 million jury verdict last year in favor of PanOptis for 4G LTE patent

infringements by Apple, a recent jury retrial including directions to consider requirements

for FRAND licensing terms has revised the award to $300 million. Apple says It

plans to appeal.

It is OEM conduct that unlevels the playing field

Contentions

about royalty charges are as much about the differences in licensing fees among

licensees as they are about the level of charges overall. It is these

differences that effect competition among OEMs.

The absolute

costs of patent licensing fees have never had much effect on overall market demand

because aggregate royalties paid by OEMs are modest in comparison to their handset

prices and revenues. While many OEMs,

including larger ones like LG in recent years, struggle for profitability, it

is the disparities in the amounts paid—or not paid—for licensing that can cause

significant competitive disadvantage or advantage among smartphone and other

device OEMs. For example, all manufacturers have to pay somewhat similar prices

for commodities such as batteries and memory chips, and European value added

taxes are levied at exactly the same rate on all manufacturers’ devices sold,

at national rates ranging from 17 percent to 27 percent.

While the

onus is upon licensees to be non-discriminatory in their licensing charges, it

is OEMs implementing SEP technologies that push for the inequalities. All the

major licensors publish rate cards and would willingly license to all OEMs at

those prices. However, major licensees such as Apple are formidable counterparties

in licensing negotiations and disputes. They have the motivation, deep pockets

and clout to force burdensome and drawn-out litigation, and yet can offer

enticements such as substantial cash lump sums up-front for settlement at low

effective royalty rates. Other OEMs have found it advantageous to hold out from

making any royalty payments for years under the rationale that litigation is

cheaper, even if it only delays eventual payment of FRAND royalties.

While for

many years the debate on FRAND was largely about what might be a fair and

reasonable rate for individual licensors in general, and for all of them in

aggregate, SEP litigation is increasing about discriminatory pricing. Unacceptable

versus acceptable discrimination (i.e. differences in royalty pricing for

different licensees) apparently hinges on whether different licensees are deemed

“similarly situated.” It was a key question in selecting “comparable licenses”

in TCL v. Ericsson, as it is in other disputes. This is still work-in-progress

in the courts.

Expanding the royalty base with licensed sales in IoT

My royalty

yield figures are conservative because they are based on the denominator of

mobile phone sales revenues which does not includes any sales revenues from

other cellular-enabled products including tablets, PC data sticks and IoT

devices. The inclusion of any such revenues would reduce royalty yields

further. With IoT becoming more significant in mobile communications in recent

years, omitting the increasing revenues for those devices from the denominator

of my royalty yield calculations makes my yield curve the above graphic an

increasingly conservative depiction of how low royalty charges are.

Measuring

and assessing whether royalty charges are FRAND or burdensome overall is more

complex beyond phones where the royalty yield was a simple and useful metric. Other

devices range from simple sensors to refrigerators, cars and industrial

equipment. The prices for these and the value they derive from cellular

connectivity varies enormously.

Non-phone

devices are commonly licensed, but sales of these and licensing revenues on

them have been relatively small. Mobile phones continue to dominate numbers of

cellular devices sold and licensed, but the proportion of non-cellular devices

has gradually increased. According to GSMA Intelligence, the percentage total cellular

network connections that are “machine-to-machine” increased from 2.7 percent of

6.9 billion worldwide in 2013 to 17.4 percent of 10 billion in 2020. The percentages of non-phone device sales,

upon which royalties are due, would be higher in these growing markets because

it is the accumulated sales of devices over several years that drive the total

numbers of connections.

With the anticipated growth in IoT including 5G and applications such as connected cars, some analysts, including JP Morgan in a June 2021 equity research report, project significant non-smartphone revenues: for example; “an estimated ~$1 bn of the ~$6.5 bn of QTL revenue being derived from non-handset license royalties.”

Qualcomm Technology Licensing revenue breakdown

Increased SEP pooling makes sense, but buyers cartels are anticompetitive

I have already written

here that the voluntary option of one-stop-shopping for patent licenses in IoT makes sense to minimize the transaction costs in

licensing with dozens of patent owners and thousands of licensees with a wide

variety of applications.

However, initiatives

to form buyers’ groups (aka Licensing Negotiation Groups) that would

“negotiate” royalty rates from licensors collectively and, in effect, exclusively

on behalf of IoT implementers would harm the increasing stability achieved in

FRAND licensing. These monopsony cartels would have dire anticompetitive effects.

As noted by a couple of commentators: “while implementers should be consulted about the

reasonableness of standard’s technology aggregate price, the final pricing

decision should better be left to SEP owners…. Permitting companies that have not developed and do not own

technology to decide on its price would effectively resemble an expropriation

of technology, making SEP owners rightfully sceptical about participating in

such joint negotiations.”

Even patent pools like

MPEG LA’s for H.264 video SEPs—with participation from some major patent owners

who are also major OEM licensees—tend to depress royalty rates significantly below

what would be and is charged bilaterally. All well and good, maybe, for voluntary

participants (as the law requires) with mixed business models including patent

fee generation and standards-based product supply, but totally unacceptable compulsorily

for licensors, or as the only way licensees would be obliged to agree to

anything. In the case of Bluetooth and DOCSIS licensing, pool rates have been

driven down to royalty-free levels, which means that the product markets are

the only way to make money from patented technologies in those standards.

All suppliers need sanctions against non-payers

In product

and service trading, if a customer does not pay for what it receives, its

suppliers will soon stop supplying. Not so with patented technologies. The

published standards documents, patent filings and SEP declarations reveal

technologies and their application openly to all. The only way a patent holder

can withhold supply of its intellectual property is through an injunction. But

these are notoriously longwinded and difficult to obtain—if they can ever be

obtained at all— particularly for patents that have been declared standard essential

by their owners. Europe has the well-established Huawei v. ZTE framework for determining under what

conditions and developments injunctions can be applied for and then issued. The

direction of US public policy on this matter is unclear with President Biden’s executive order asking the Justice and Commerce

Departments to reconsider the previous administration’s position that patent

holders have the right to seek injunctions against potential SEP licensees.

Fair and calmer conditions ahead

For now,

the outlook in FRAND licensing appears relatively peaceful. In addition to the

numerous agreements that are negotiated and licensed without dispute, recent

FRAND licensing settlements following litigation between Ericsson and Samsung, InterDigital and Xiaomi and Ericsson and TCL, signal increasing calm in

smartphone licensing. For example, with the US District Court’s FRAND-licensing

determinations for 2G, 3G and 4G LTE in TCL v. Ericsson unanimously and entirely

vacated on appeal, the parties have subsequently settled confidentially rather

than go to retrial with a jury.

A licensing

agreement at the car OEM level —following years of litigation between Nokia and Daimler and an EU antitrust complaint about

where in the supply chain SEPs should be licensed—is a major breakthrough in

the way cars and their components are licensed. This bodes well for dealing

with the complexities elsewhere in IoT

licensing, with

numerous different applications, devices and component manufacturers and OEMs. However,

this is still only the very beginning of that saga.

This article was originally published in RCR Wireless on 3rd September 2021.

Tuesday, 3 August 2021

Who Benefits from the Fruit of Research from Human Cells? Civil Rights Attorney Representing Henrietta Lacks Family

In a fascinating turn of events, Ben Crump, the prominent civil rights attorney who represented the family of Treyvon Martin and Breonna Taylor, is representing the family of Henrietta Lacks, a deceased African-American woman. Ms. Lacks’ cells were used without her consent to develop a cell line at Johns Hopkins Hospital (extracted from her in 1951). There is a book and movie concerning her story. According to Johns Hopkins Medicine’s website honoring Ms. Lacks:

Today, these incredible cells— nicknamed "HeLa"

cells, from the first two letters of her first and last names — are used to

study the effects of toxins, drugs, hormones and viruses on the growth of

cancer cells without experimenting on humans. They have been used to test the

effects of radiation and poisons, to study the human genome, to learn more

about how viruses work, and played a crucial role in the development of the

polio vaccine.

. . . Over the past several decades, this cell line has contributed to many medical breakthroughs, from research on the effects of zero gravity in outer space and the development of the polio vaccine, to the study of leukemia, the AIDS virus and cancer worldwide.

The website also states:

In 2013, Johns Hopkins worked with members of the family and

the National Institutes of Health (NIH) to help broker an agreement that

requires scientists to receive permission to use Henrietta Lacks’ genetic

blueprint, or to use HeLa cells in NIH funded research.

The committee tasked with deciding who can use HeLa cells now

includes two members of the Lacks family. The medical research community has

also made significant strides in improving research practices, in part thanks

to the lessons learned from Henrietta Lacks’ story.

Moreover, the legal area and practices have developed since

1951, including the development of informed consent laws. The website also notes that John Hopkins was

one of the few hospitals that accepted poor African Americans as patients in 1951.

The likely defendants will include pharmaceutical and biotechnology companies

as well as John Hopkins. This case—assuming

it survives many legal challenges and is not settled relatively early (those are big “ifs”)—could

result in some very interesting law on the merits that may be challenging to

the biotechnology and pharmaceutical industries.

In 1990, the California Supreme Court basically decided in Moore v. Regents of the University of California that a patient did not retain a

property interest in tissue extracted from him.

Notably, his cells were also used to develop a cell line. The majority’s decision was influenced by

prudential concerns, including expressed fear about impeding the development of

the promising biotechnology industry. Importantly,

the case was decided when the biotechnology industry was arguably quite young

and the reasoning in that case was based on some factors that may not hold true

today—due to changes in the law, the development of technology, and changing

expectations and practices. Other courts

in the United States, in deciding similar issues, have basically stated that equity (unjust enrichment) may provide hope for some compensation to the party whose cells have

been utilized by researchers. A rejection

of Moore would have interesting implications for the field and the

preservation and protection of human dignity.

The timing of the filing of the lawsuits is interesting

because my guess is that public opinion of the pharmaceutical/biotechnology industry

is relatively high in the United States given the development of the vaccines for COVID-19. However, the continuing disaster of the

failure to get enough vaccines to the Global South and other parts of the world will result in additional human death and suffering, including the proliferation of variants which may evade

vaccines. This could turn the tide of

public opinion in the United States—along with high pharmaceutical prices—and result in additional pressure

to settle.

Subscribe to:

Posts (Atom)