How Should We Measure Output and Productivity?

Let's now turn to the second question of how to best measure output and productivity. While there are some subtleties in measuring oil output, we know how to count barrels of oil. Measuring the overall level of goods and services produced in the economy is fundamentally messier, because it requires adding apples and oranges—and automobiles and myriad other goods and services. The hard-working statisticians creating the official statistics regularly adapt the data sources and methods so that, insofar as possible, the measured data provide accurate indicators of the state of the economy. Periods of rapid change present particular challenges, and it can take time for the measurement system to adapt to fully and accurately reflect the changes in the economy.

Let's now turn to the second question of how to best measure output and productivity. While there are some subtleties in measuring oil output, we know how to count barrels of oil. Measuring the overall level of goods and services produced in the economy is fundamentally messier, because it requires adding apples and oranges—and automobiles and myriad other goods and services. The hard-working statisticians creating the official statistics regularly adapt the data sources and methods so that, insofar as possible, the measured data provide accurate indicators of the state of the economy. Periods of rapid change present particular challenges, and it can take time for the measurement system to adapt to fully and accurately reflect the changes in the economy.

The advance of technology has long presented measurement

challenges. In 1987, Nobel Prize–winning economist Robert Solow quipped that

"you can see the computer age everywhere but in the productivity

statistics."6 In the second half of the

1990s, this measurement puzzle was at the heart of monetary policymaking.7 Chairman Alan Greenspan

famously argued that the United States was experiencing the dawn of a new

economy, and that potential and actual output were likely understated in

official statistics. Where others saw capacity constraints and incipient

inflation, Greenspan saw a productivity boom that would leave room for very low

unemployment without inflation pressures. In light of the uncertainty it faced,

the Federal Open Market Committee (FOMC) judged that the appropriate risk‑management

approach called for refraining from interest rate increases unless and until

there were clearer signs of rising inflation. Under this policy, unemployment

fell near record lows without rising inflation, and later revisions to GDP

measurement showed appreciably faster productivity growth.8

This episode illustrates a key challenge to making

data-dependent policy in real time: Good decisions require good data, but the

data in hand are seldom as good as we would like. Sound decisionmaking

therefore requires the application of good judgment and a healthy dose of risk

management.

Productivity is again presenting a puzzle. Official

statistics currently show productivity growth slowing significantly in recent

years, with the growth in output per hour worked falling from more than 3

percent a year from 1995 to 2003 to less than half that pace since then.9 Analysts are actively

debating three alternative explanations for this apparent slowdown: First, the

slowdown may be real and may persist indefinitely as productivity growth

returns to more‑normal levels after a brief golden age.10 Second, the slowdown may

instead be a pause of the sort that often accompanies fundamental technological

change, so that productivity gains from recent technology advances will appear

over time as society adjusts.11 Third, the slowdown may

be overstated, perhaps greatly, because of measurement issues akin to those at

work in the 1990s.12 At this point, we cannot

know which of these views may gain widespread acceptance, and monetary policy

will play no significant role in how this puzzle is resolved. As in the late

1990s, however, we are carefully assessing the implications of possibly

mismeasured productivity gains. Moreover, productivity growth seems to have

moved up over the past year after a long period at very low levels; we do not

know whether that welcome trend will be sustained.

Recent research suggests that current official statistics may

understate productivity growth by missing a significant part of the growing

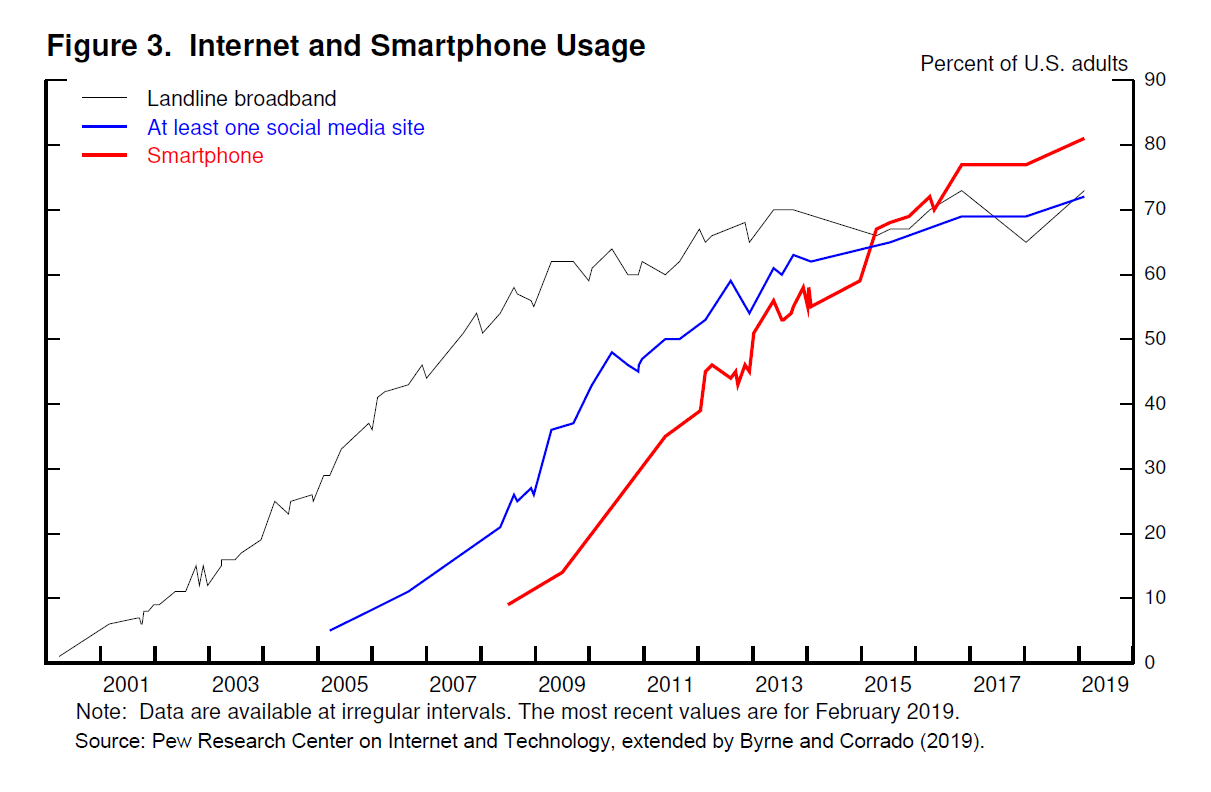

value we derive from fast internet connections and smartphones. These

technologies, which were just emerging 15 years ago, are now ubiquitous (figure

3). We can now be constantly connected to the accumulated knowledge of

humankind and receive near instantaneous updates on the lives of friends far

and wide. And, adding to the measurement challenge, many of these services are

free, which is to say, not explicitly priced. How should we value the luxury of

never needing to ask for directions? Or the peace and tranquility afforded by

speedy resolution of those contentious arguments over the trivia of the moment?

{kind=link}

Researchers have tried to answer these questions in various

ways.13 For example, Fed

researchers have recently proposed a novel approach to measuring the value of

services consumers derive from cellphones and other devices based on the volume

of data flowing over those connections.14 Taking their accounting

at face value, GDP growth would have been about 1/2 percentage point higher

since 2007, which is an appreciable change and would be very good news. Growth

over the previous couple of decades would also have been about 1/4 percentage

point higher as well, implying that measurement issues of this sort likely

account for only part of the productivity slowdown in current statistics.

Research in this area is at an early stage, but this example illustrates the

depth of analysis supporting our data-dependent decisionmaking.

The full speech is available, here. The paper concerning measuring value using volume of data, titled, "Accounting for Innovations in Consumer Digital Services: IT Still Matters," is available, here.

No comments:

Post a Comment